Consumer Sentiment Survey Spring 2026

Back to All Insights

In February 2026, A&M Consumer and Retail Group surveyed over 2,000 U.S. consumers to understand their financial outlook, spending priorities, and shopping behaviors. Results show sentiment remains cautious, with higher-income households showing signs of pulling back while lower-income groups are modestly recovering. Additionally, consumers are changing the way they shop for value, while loyalty and discovery are being tested by the increased presence of AI in customer journeys.

- A Narrowing Gap in Financial Confidence and Behavior

Higher-income consumers are becoming more cautious across earning, spending, and saving, while sentiment among lower-income households is stabilizing and showing early signs of recovery. - Smarter Shopping, Not Just Cheaper Choices

Consumers are pursuing value by changing their shopping behaviors, trip occasions and retailer choices, while finding better experiences in lower-priced retailers and store brand products, satisfying affordability without sacrificing standards. - Intentional Consumption and Selective Trade-Ups

Consumers are buying less while selectively trading up for products that deliver on performance, quality, longevity or premium experiences. “Intentional consumption” prioritizes fewer, higher-value purchases over volume-driven spend. - Loyalty is Being Tested

Price, convenience, and novelty are overtaking traditional brand affinity, with consumers increasingly open to switching products and brands that suit their changing lifestyles and desire to experiment, particularly among younger demos. - Shopping is Going ‘Phygital’

Consumers are increasingly using digital channels and AI to research and discover products but a large segment still rely on physical stores to make a final decision. The blend of online-driven discovery and store conversion makes a seamless omnichannel experience imperative to win over consumers.

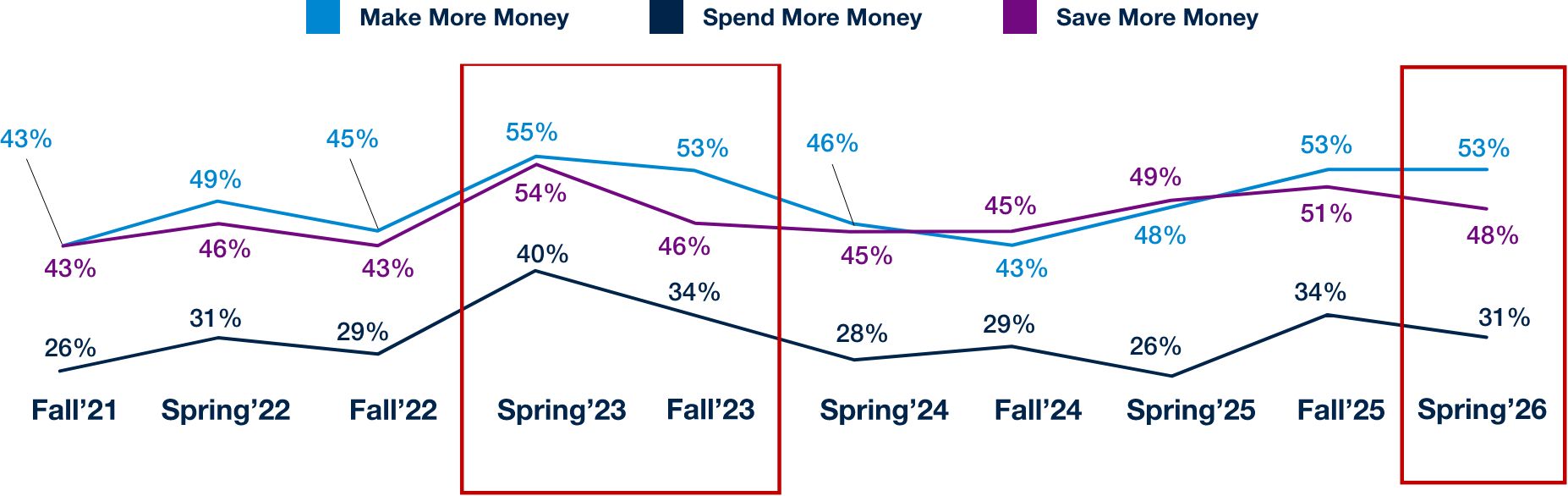

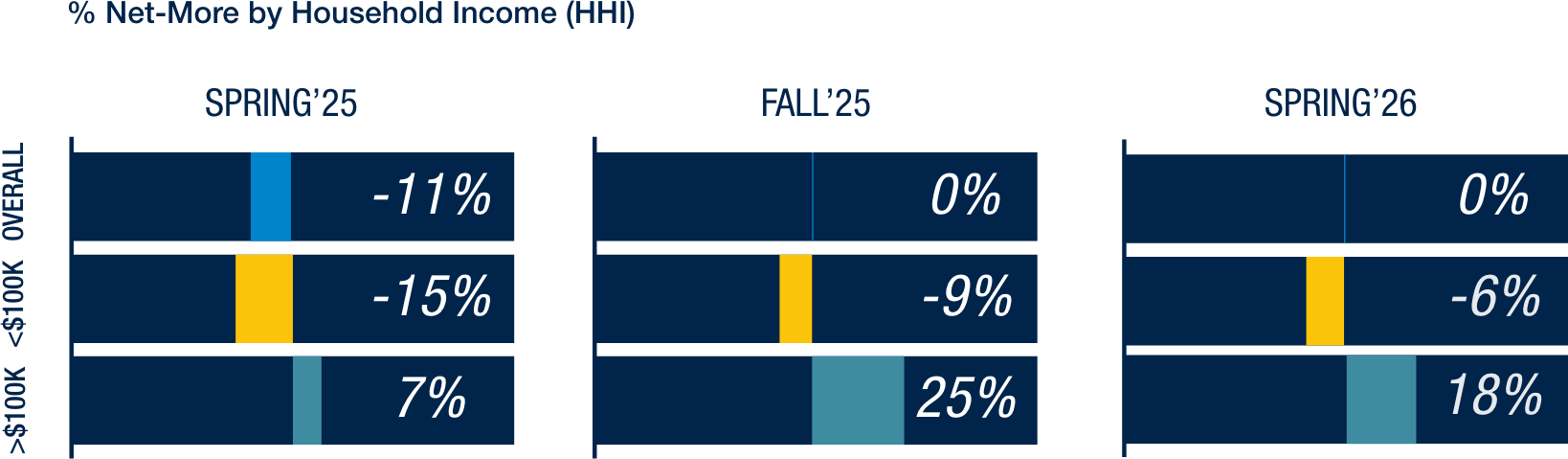

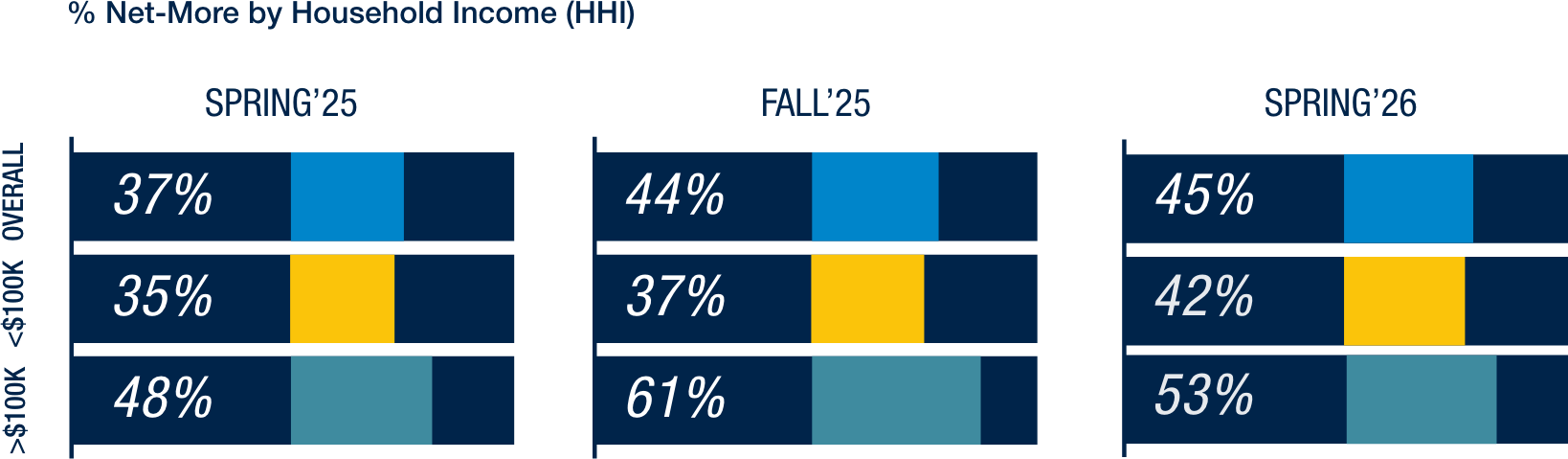

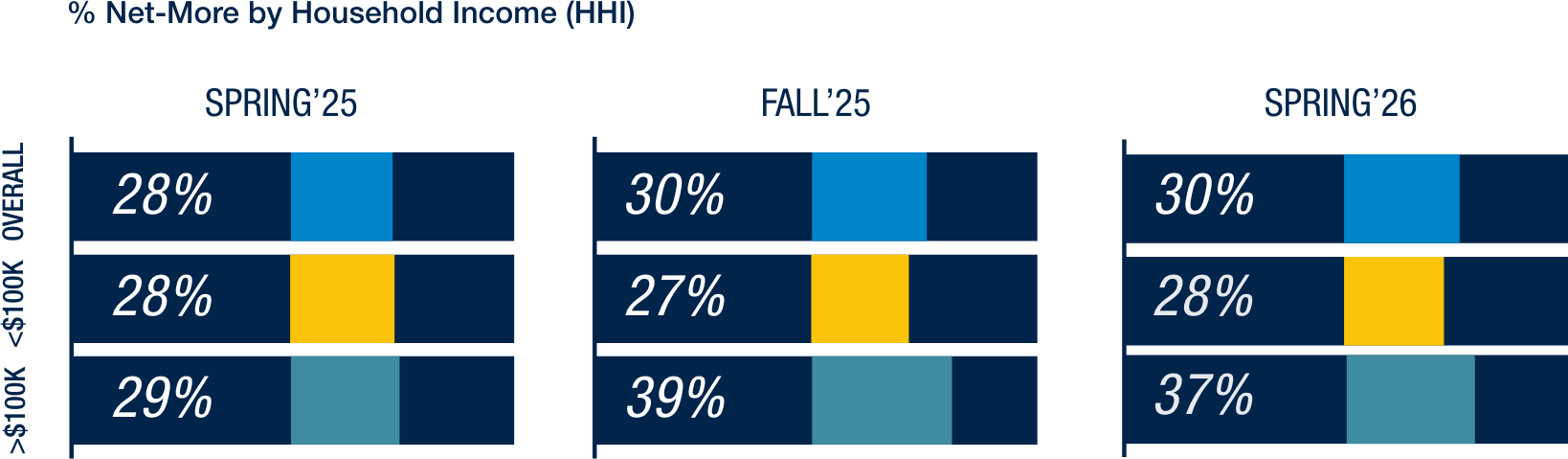

As earning expectations hold strong, the historic link between making more and spending more is breaking down. Higher-income households (HHI >$100K), who drove optimism in Fall ’25, are pulling back across all three dimensions: make (-8% vs. Fall ‘25), spend (-7%), and save (-2%). We observed the same pattern in Fall 2023, when a surge in consumer confidence quickly reversed. Meanwhile, lower-income households (HHI <$100K) are quietly gaining ground, with earn expectations climbing to 42% net-more and spend sentiment ticking upward. Lower-income consumers are slowly emerging from financial pressure while higher-income households are becoming more cautious, slowing down their anticipated spending.

Consumer Financial Plans – Historical Trends

Consumer Financial Plans for Next 6 Months

- SPEND

- MAKE

- SAVE

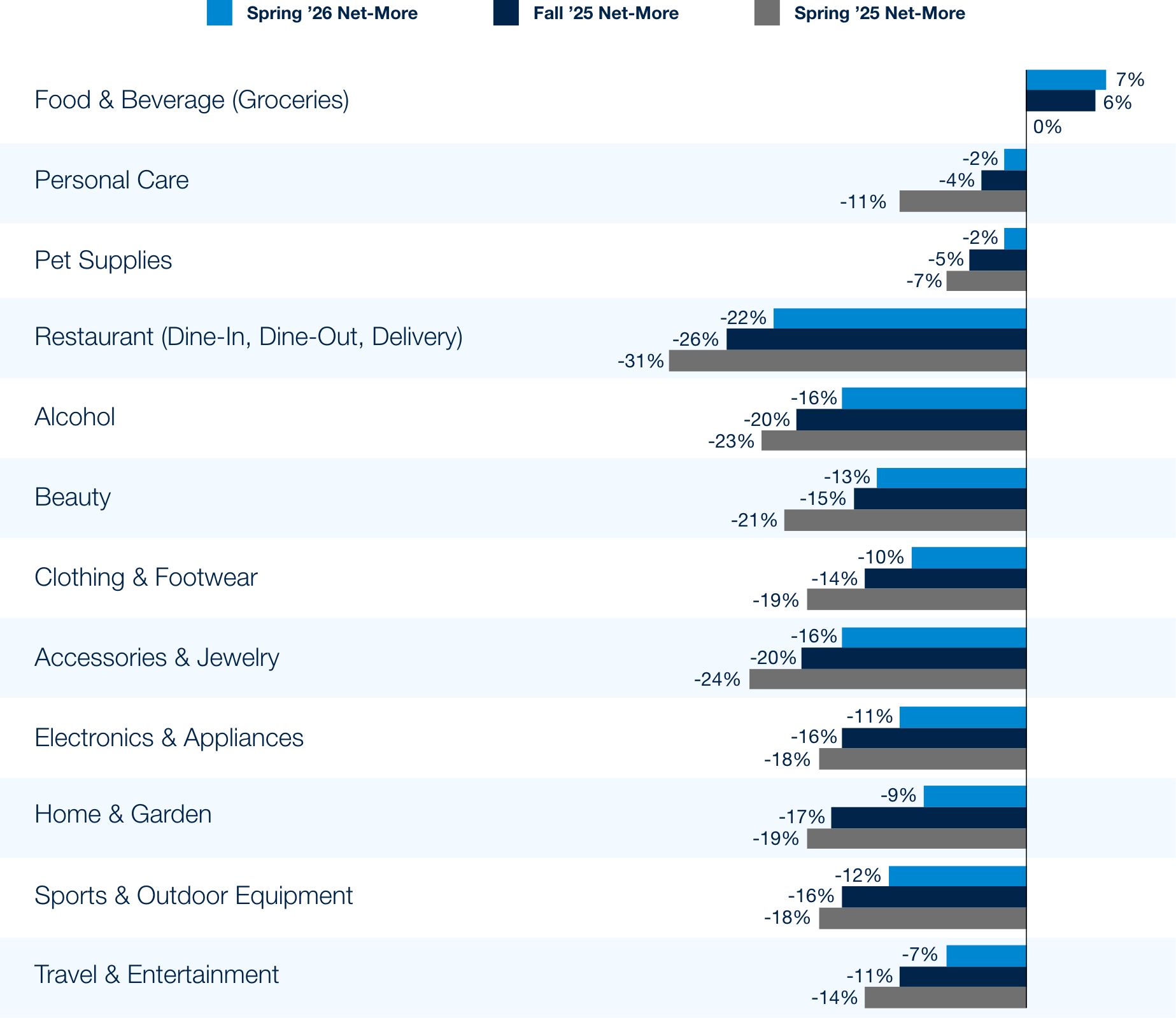

Category Spending Plans

Overall and category spending plans show a similar pattern to Fall ’25. Consumers are showing continued optimism across essential and discretionary categories compared to previous cycles. Grocery continues to be an area where consumers expect to spend more, lifted by inflation expectations, while pulling back on remaining categories. Additionally, non-discretionary categories experienced 4-8 percentage point improvements in net-more compared to Fall ‘25, such as alcohol, clothing & footwear, and home & garden.

Consumer Spending Plans by Category

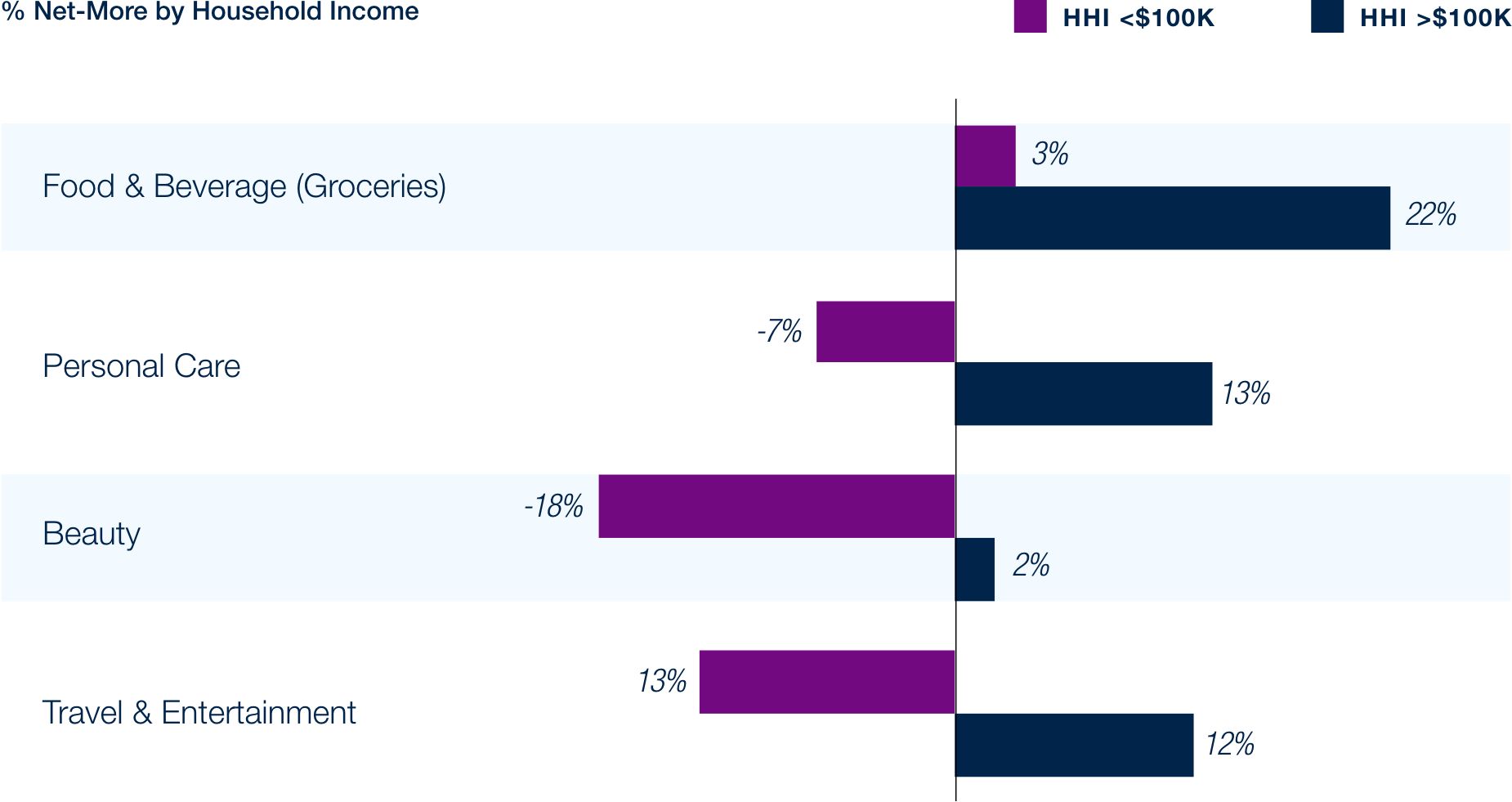

Despite most categories holding an overall negative net-more spend expectation, higher-income households are notably more optimistic. This spring, spending expectations in grocery, personal care, beauty, and travel & entertainment diverged by 19-25 percentage points between low and high household income consumers.

Consumer Spending Plans by Household Income

Consumers’ Shopping Habits Focus on Value

Consumers aren’t just spending less — they’re spending more deliberately. Across all income levels, people are hunting for value in different ways than before: shifting to private label items and shopping at discount grocers, simplifying beauty routines, and prioritizing essential clothing over discretionary apparel purchases.

GROCERY

In grocery, consumers are cutting costs by shopping at lower-cost stores instead of just switching to cheaper brands. Shoppers are also embracing private label products, now viewed as quality alternatives rather than compromises.

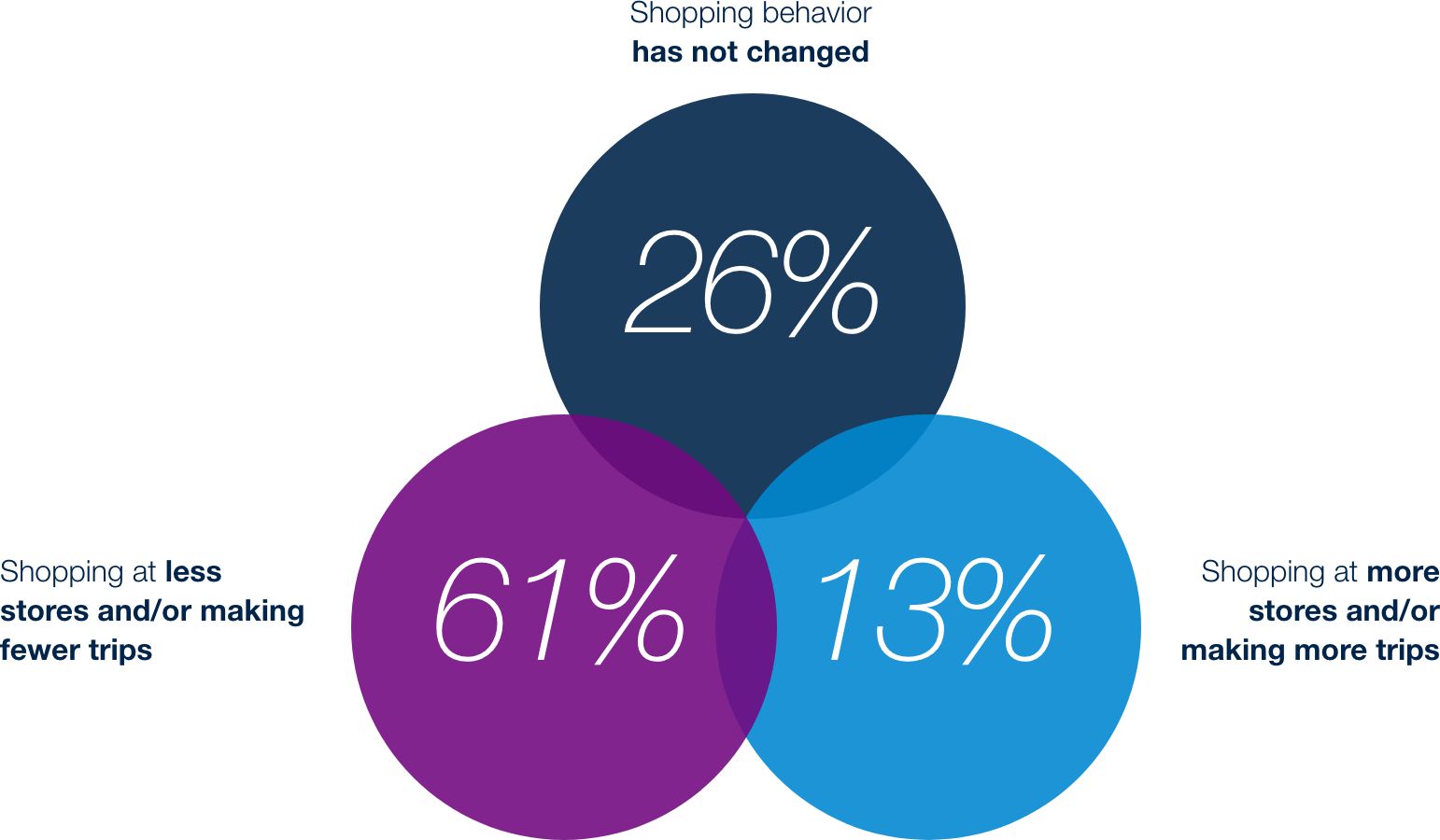

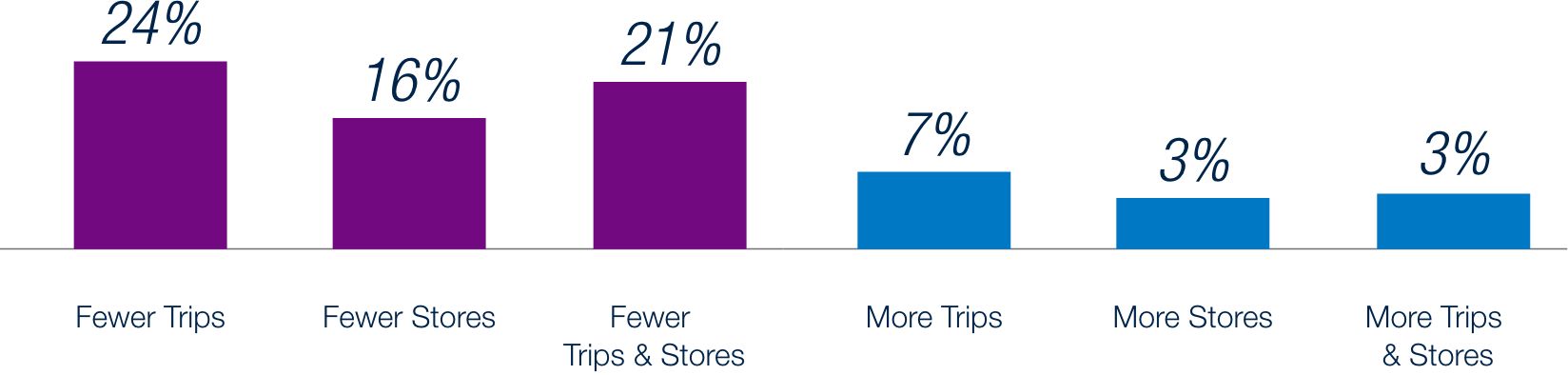

Overall, 61% of consumers are consolidating their grocery trips while 13% are expanding them. In both groups, 50-60% are shifting towards lower priced retailers in search of more affordable options. Together, these behaviors signal a meaningful shift in how consumers approach grocery shopping; whether consolidating trips toward lower-priced retailers or adding them into routines, consumers are actively seeking value.

Consumer Shopping Behavior in the Last 6 Months

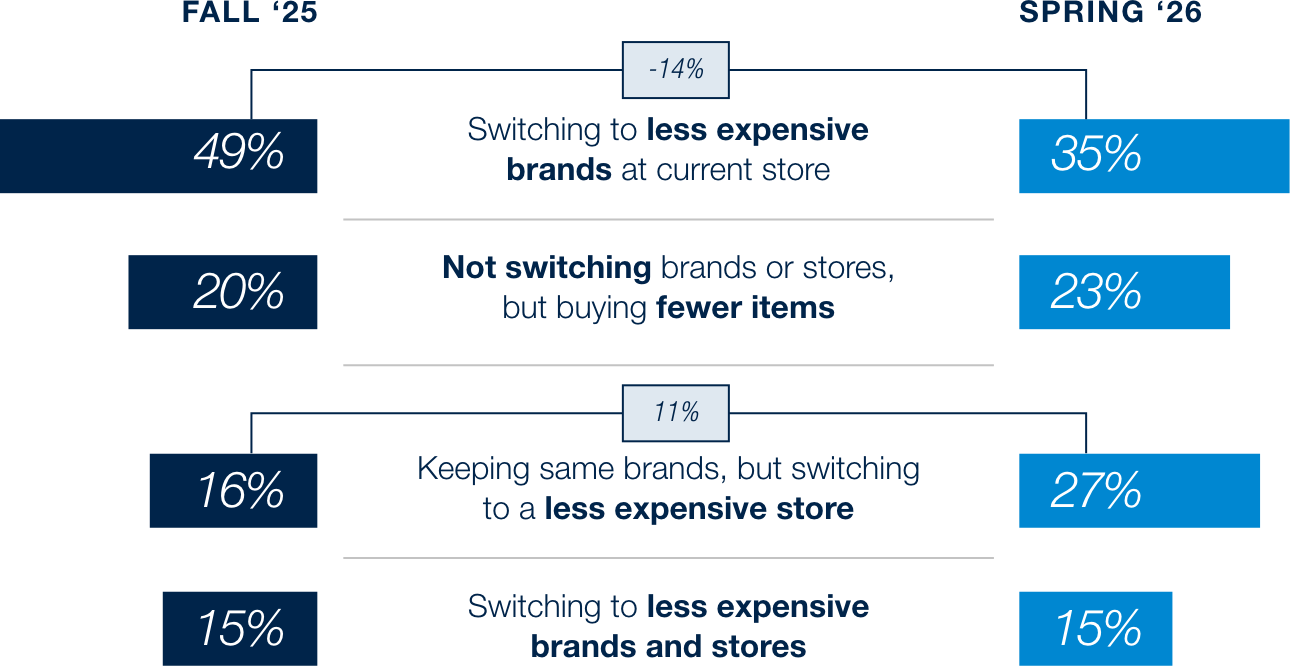

Grocery shoppers are shifting how they seek value: 35% plan to switch to less expensive brands, down from 49% in Fall ’25. Another 27% are keeping their brands but switching to a less expensive store, up from 16% in Fall ’25. A new trend is emerging – consumers are moving away from trading down on brands and toward trading down on retailers.

Consumer Approach to Reducing Grocery Spend

As consumers look for value, perceptions of lower-priced grocers have improved. These retailers are increasingly viewed as viable alternatives to traditional grocers with switching behavior more likely to stick the longer consumers pursue these options and walk away with a positive experience.

Consumer Perception of Lower Price Grocers

(LPG) vs Traditional Grocers (TG)

Agree Rate by HHI

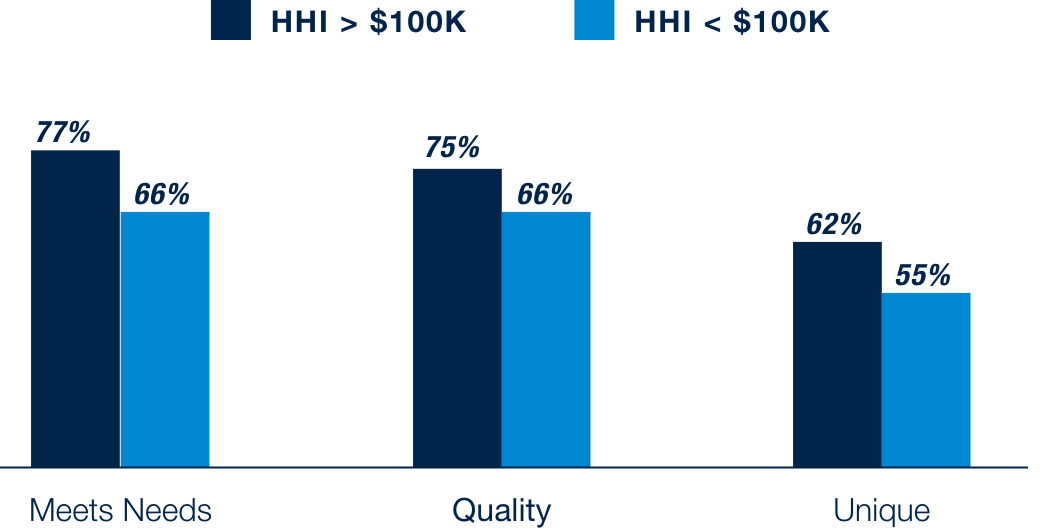

Higher-income households are among private label’s biggest converts. 77% say store brands meet their dietary and lifestyle needs and 75% rate quality as equal or better – higher than the overall average. Private label has shed its trade-down reputation, even at the top of the income spectrum.

Consumer Perceptions of Store Brand vs

National Brand Groceries

Store Brand groceries…

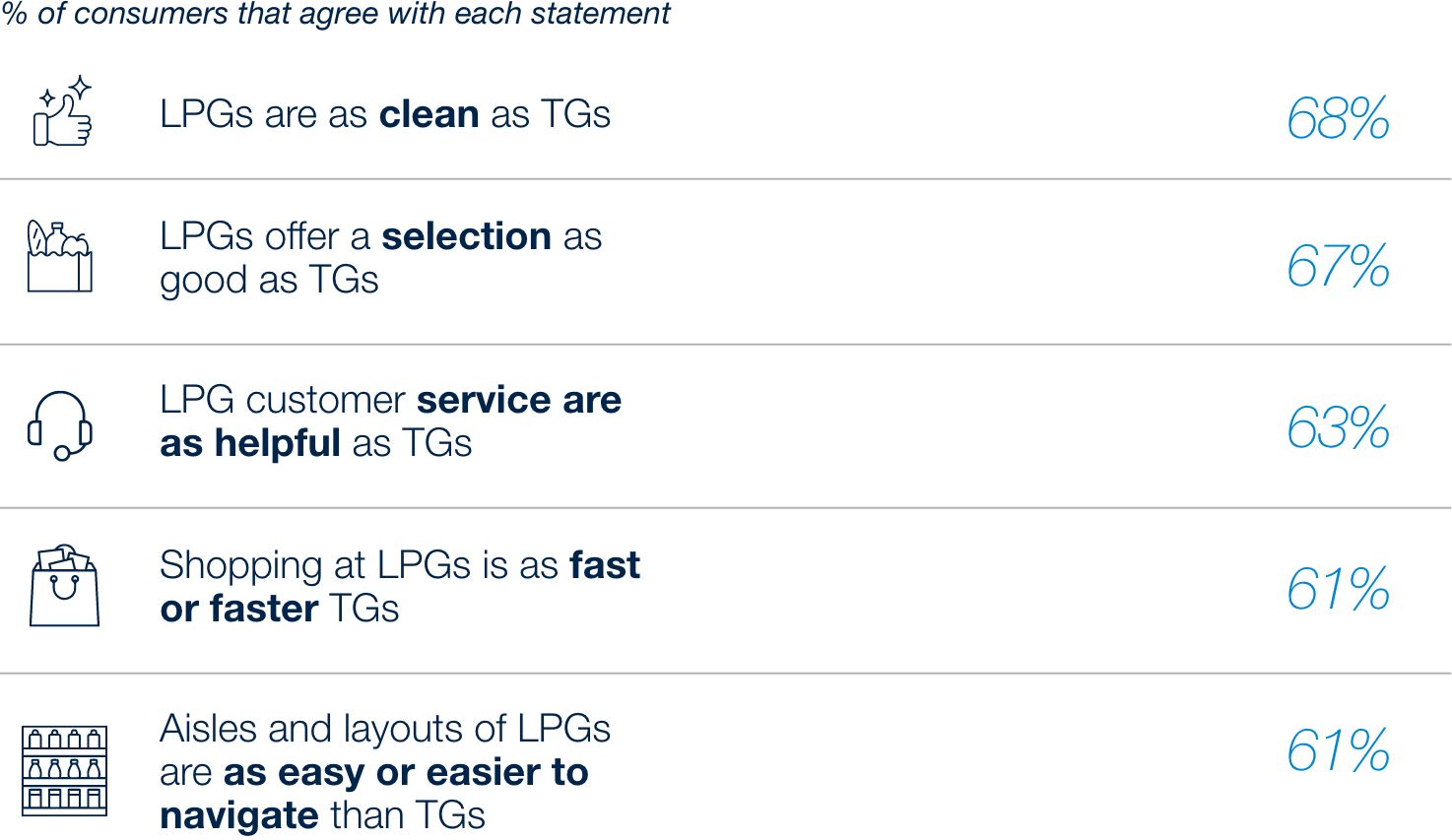

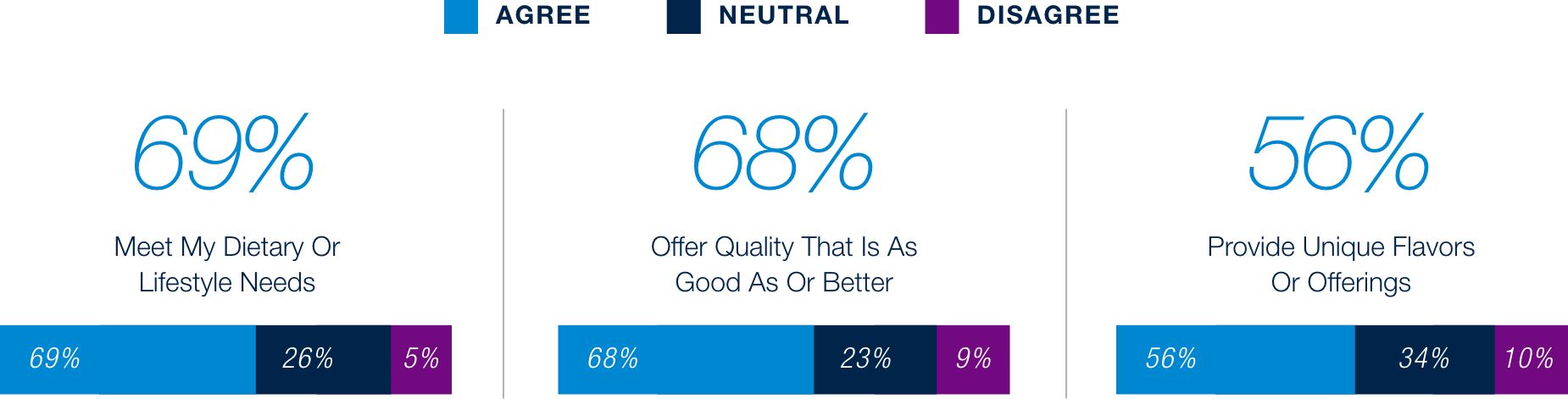

Consumers are also growing more confident in private label options. Affordability is a clear draw – 85% of consumers agree that store brands are more affordable than national brands – but the appeal goes beyond the price tag. 68% of consumers consider quality to be equal to or better than national brands and 56% appreciate the unique flavors and offerings, redefining how private label brands deliver on common food & beverage purchase drivers.

BEAUTY

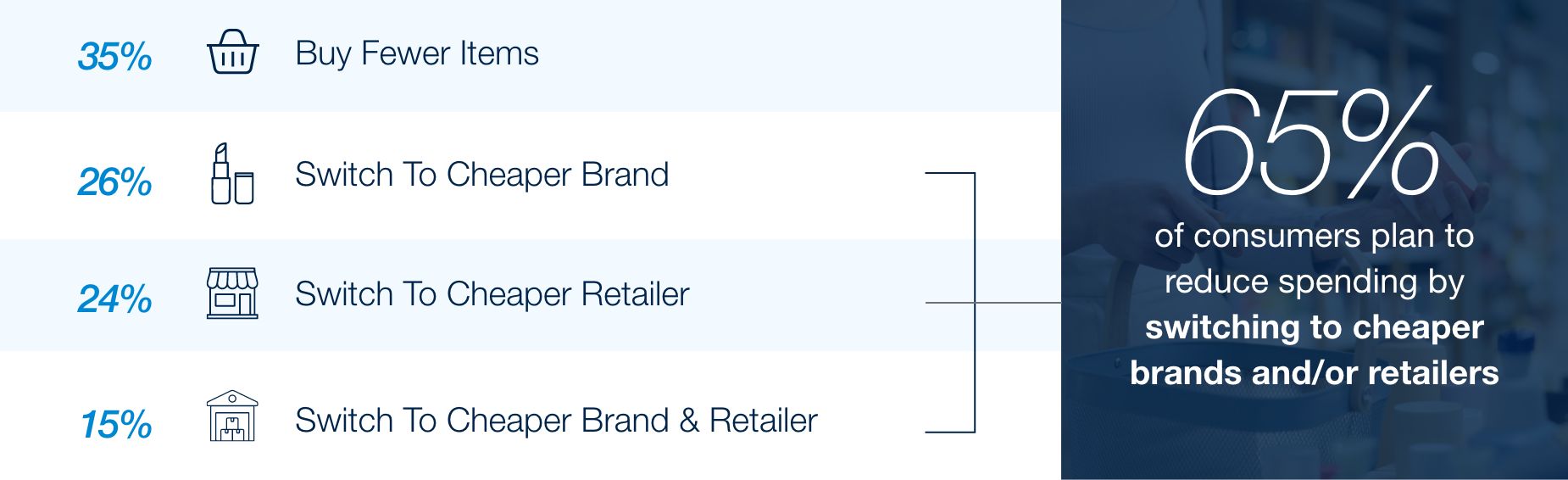

In beauty, consumers are streamlining routines and concentrating spend on core categories – and the value-seeking mindset driving this shift is reshaping how all shoppers approach the aisle. One in four beauty consumers identifies as cost-conscious, and their behavior reflects clear trade-offs. 35% are buying fewer items outright, while 65% are switching brands, retailers, or both in search of lower prices. The pressure on brands and retailers is growing – not just to compete on price, but on perceived value at the shelf.

How Shoppers are Planning to Reduce their

Beauty Spending

Value-seeking isn’t limited to the shopper on a tight budget. Across the full respondent base, 43% have simplified their routines over the past year, using fewer steps and products overall. As baskets shrink, brands that sharpen their assortment and earn customer loyalty will be best positioned to capture remaining wallet share.

APPAREL

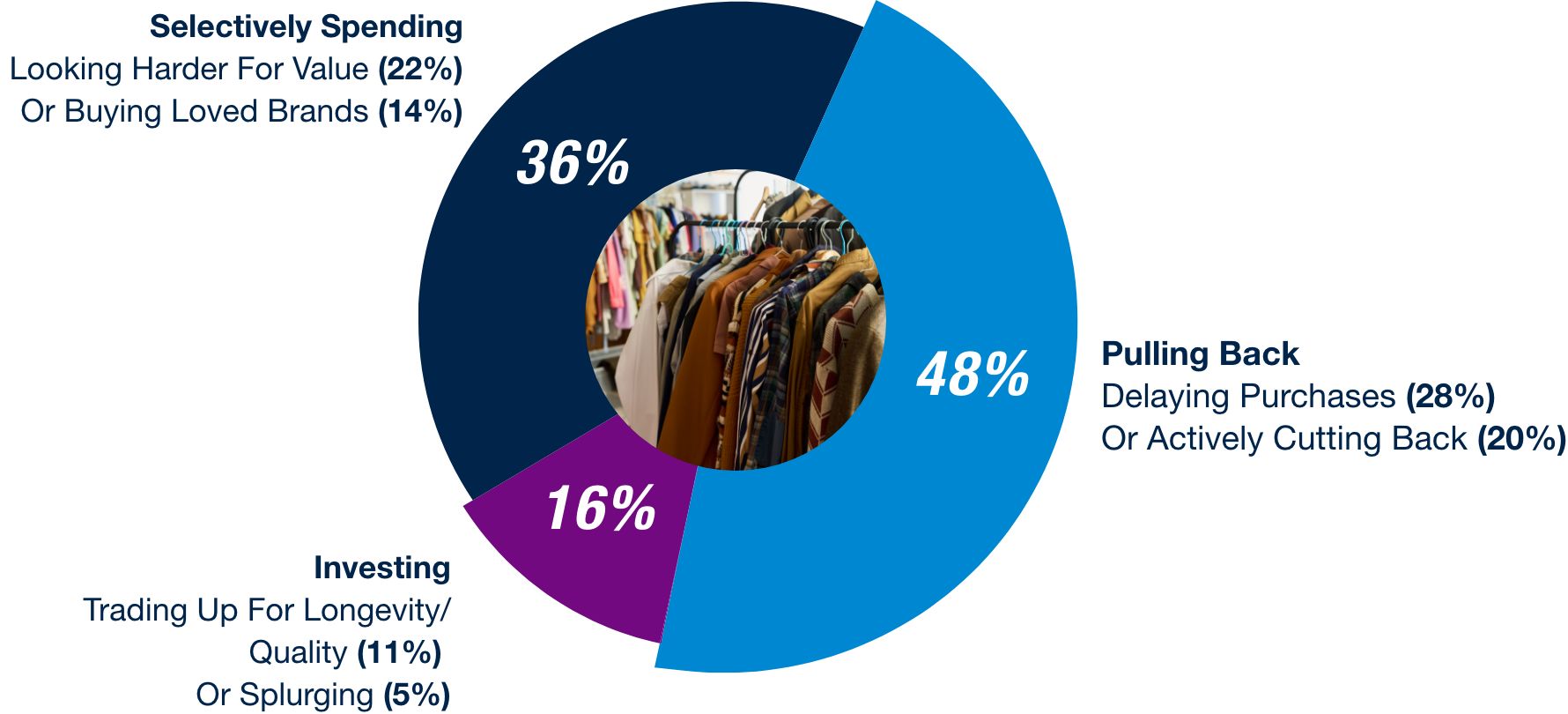

In apparel, consumers are broadly pulling back on spend, prioritizing value over volume. While lower income shoppers are tightening out of necessity, higher-income consumers are reframing their purchases as conscious investments. Nearly half of consumers are actively pulling back spend (48%), while some are prioritizing value (22%) and sticking with trusted brands (14%). Only a small group of shoppers are trading up or splurging (16%).

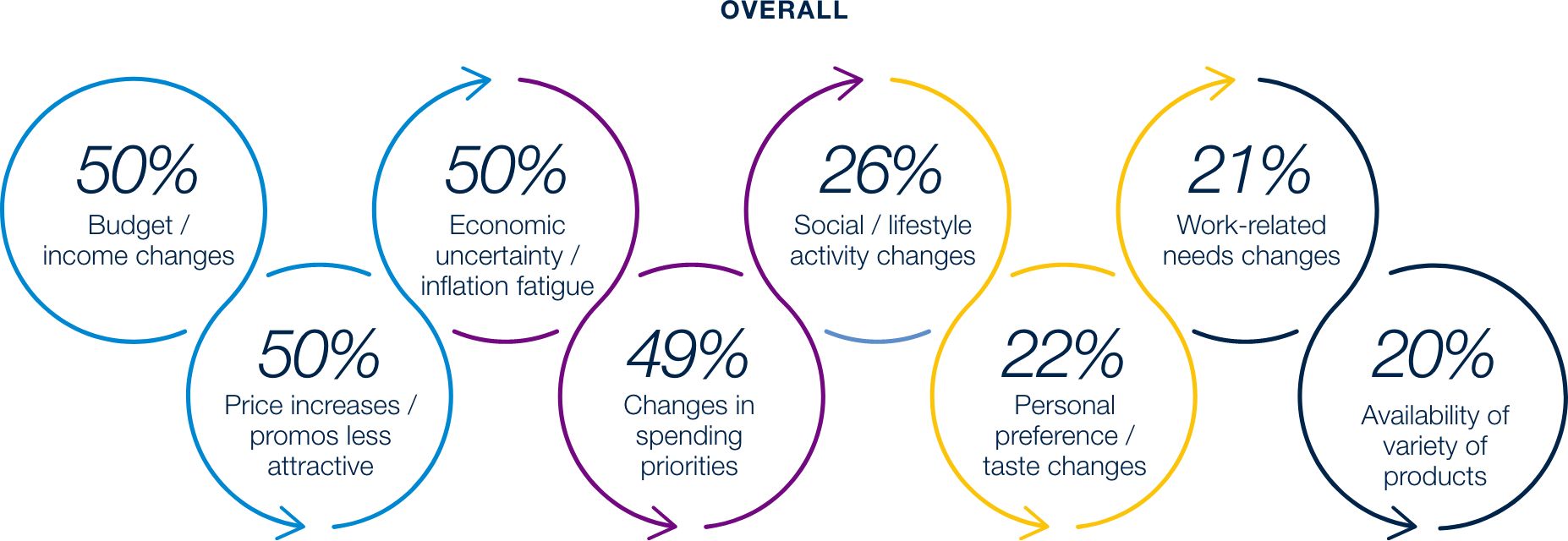

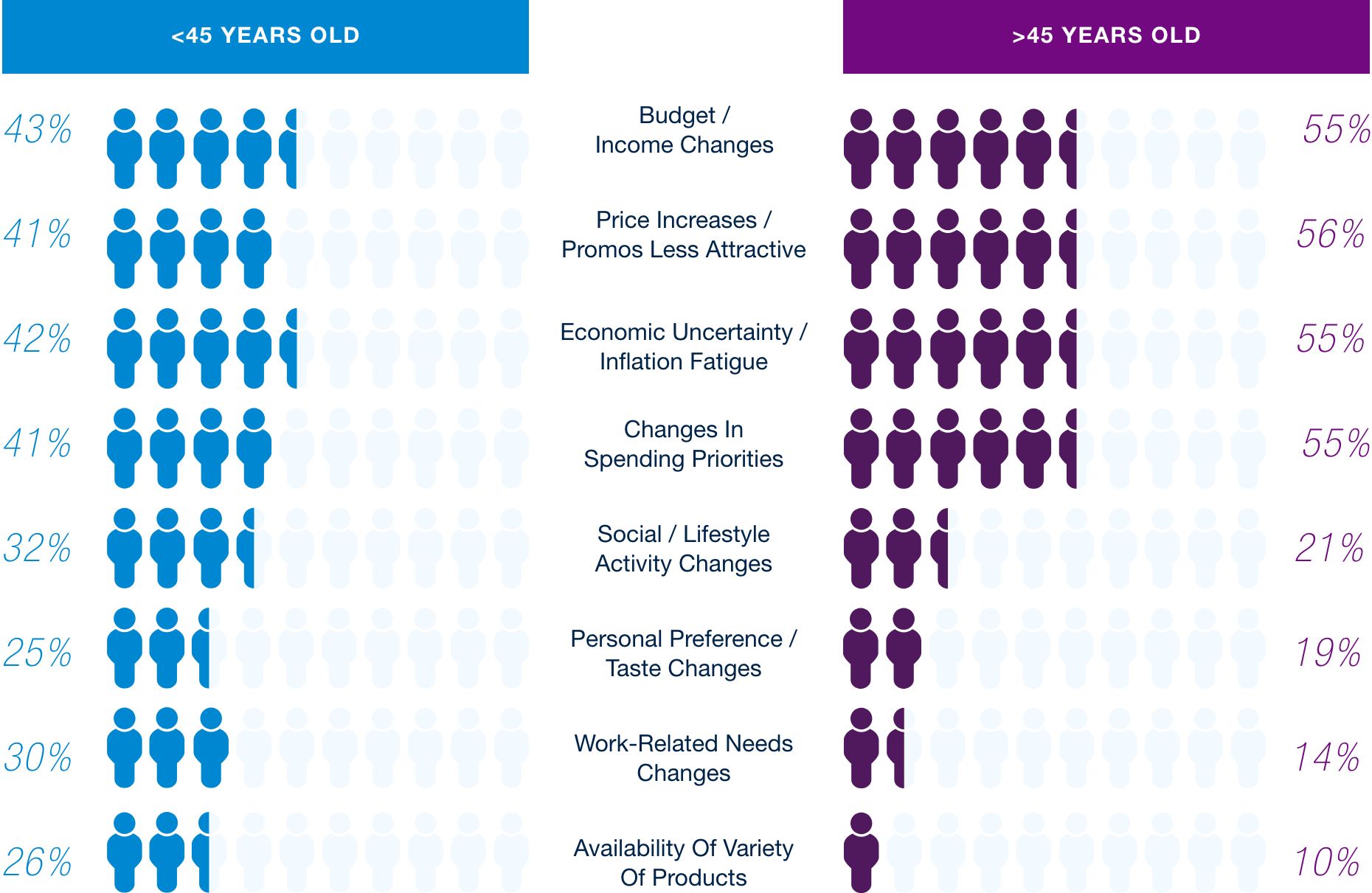

Consumers who plan to spend less in apparel cite income pressure and price changes as top drivers – but motivation diverges by age. Younger shoppers pointed to shifting work needs and spending priorities, while older consumers are driven primarily by financial pressures like budget constraints and economic uncertainty.

Older and Younger Consumers are Cutting

Apparel Spend for Different Reasons

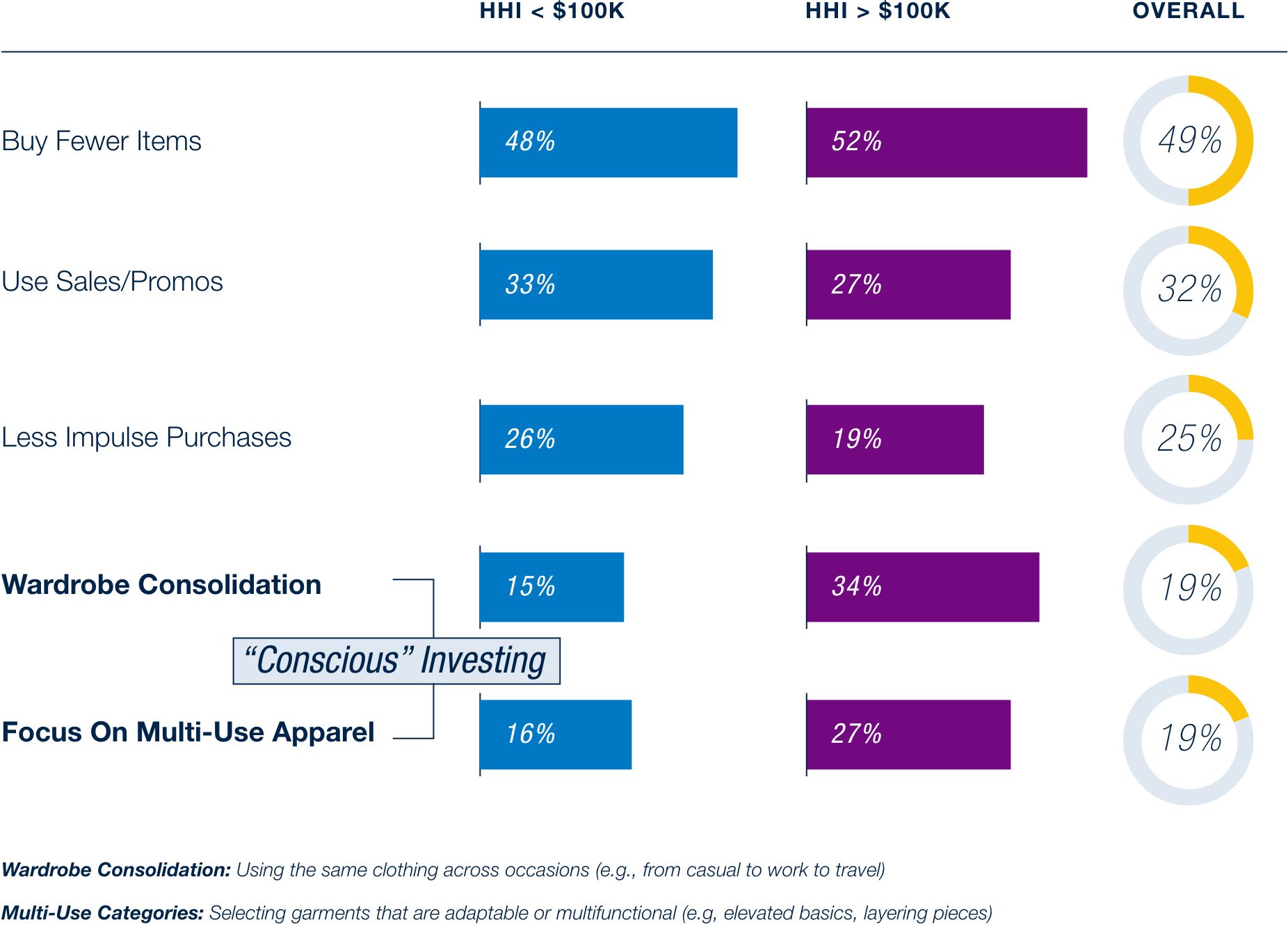

Roughly 30% of consumers expect to spend less on clothing and footwear by reducing overall volume (49%), shopping during sales & promotions (32%), and making fewer impulse purchases (25%). Consumers’ cost-cutting strategies vary by income – lower income consumers lean on traditional levers like finding promotions and reducing impulse purchases. On the other hand, higher income households are gravitating towards “conscious investing”, focusing on maximizing use and value from what they buy.

Consumer Strategies for Reducing

Spend in Clothing & Footwear

Investing Intentionally

Even as consumers broadly pull back, a meaningful share across grocery, beauty, and apparel are selectively trading up when the value feels justified. Today’s consumers aren’t simply tightening their belts – they’re making thoughtful trade-offs, pulling back in some areas while investing in products that deliver real quality and lasting value.

- Grocery

- Apparel

- Beauty

What Drives Consumers to Trade Up

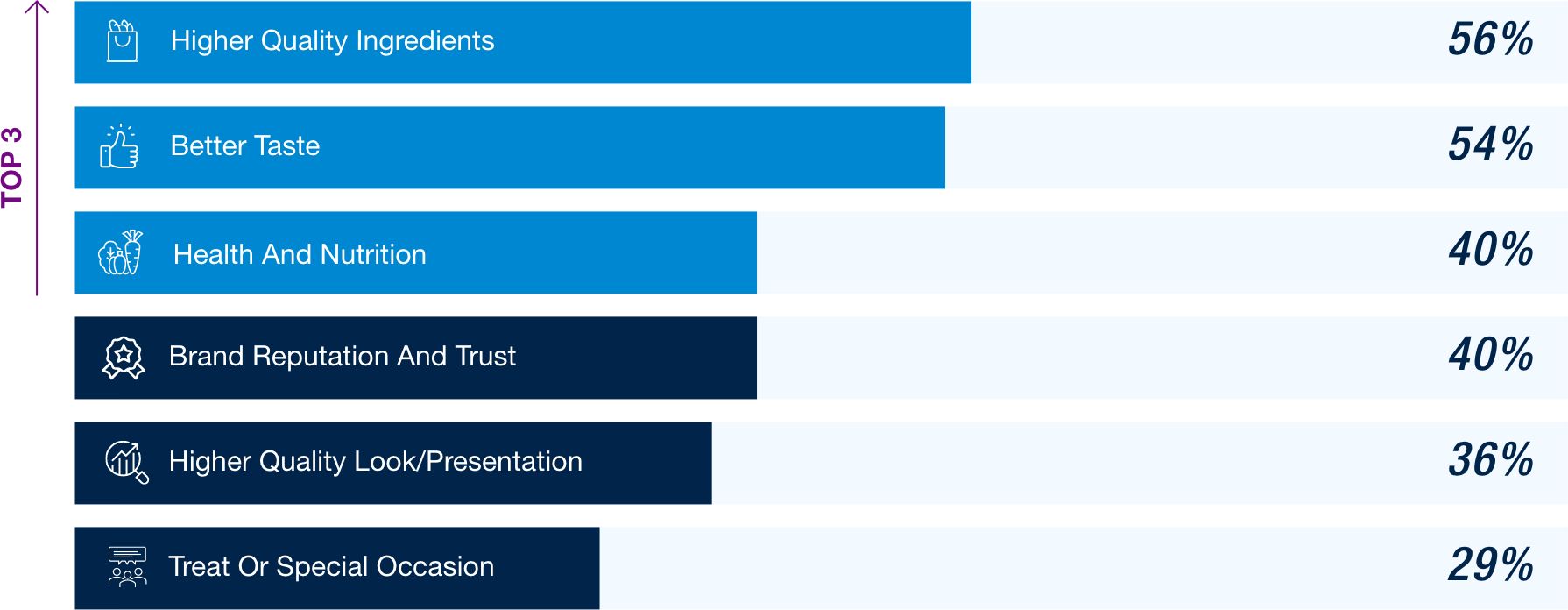

Grocery shoppers aren’t just cost-cutting across the board - around 30% report they are trading up by choosing higher-priced brands over their usual preferences. Even in a cost-conscious environment, shoppers are not uniformly trading down but instead making more deliberate choices; cutting back in some areas while prioritizing quality, taste, and preferred products in others.

What Makes “Premium Pricing” Worthwhile

When Grocery Shopping

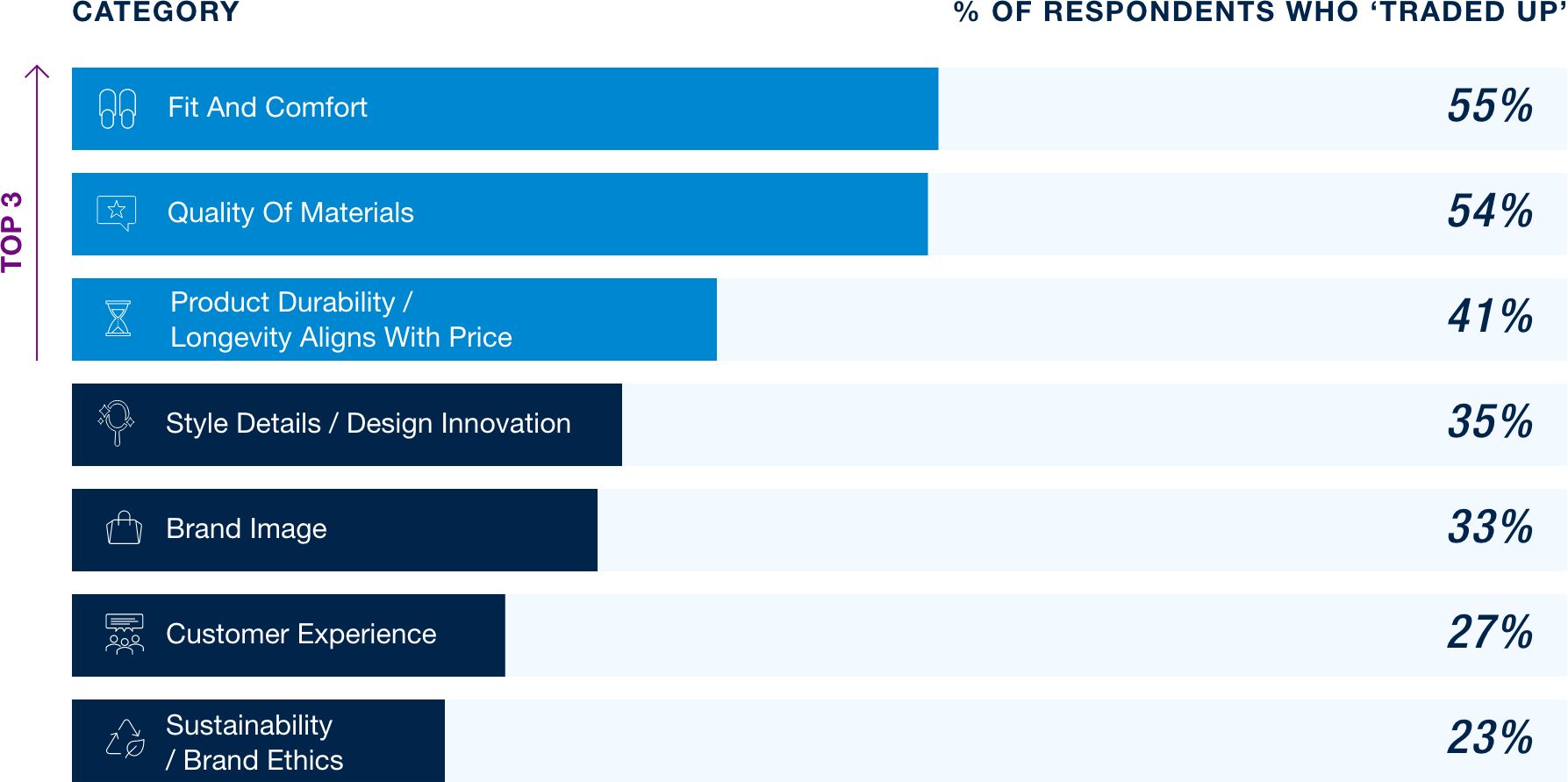

In apparel, this shows that buying less doesn’t mean buying cheaper. Trade-ups are driven by core attributes, like fit and comfort (55%), quality of materials (54%), and durability (41%). Shoppers are willing to pay a premium, but only when a product delivers on how it fits, feels, and lasts.

What Makes “Premium Pricing” Worthwhile

When Grocery Shopping

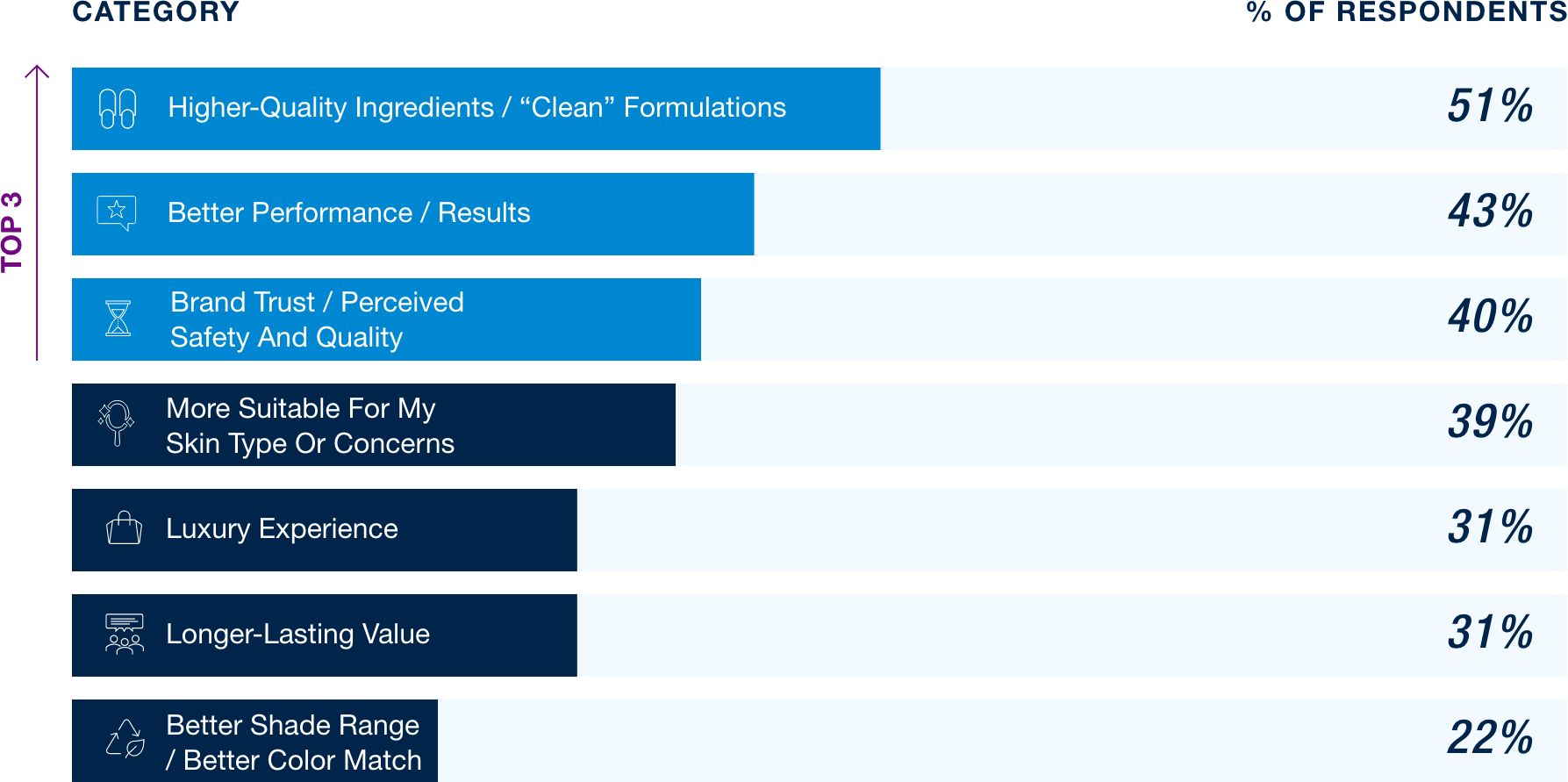

A similar dynamic is playing out in beauty. Trade-up in beauty is led by higher-quality ingredients (51%), performance (43%) and brand trust/ quality (40%), with the first two cutting across all income levels. Even as some cut back, others continue to invest in higher-priced products that deliver results.

What Makes “Premium Pricing” Worthwhile

When Grocery Shopping

Waning Loyalty

Brand loyalty is under pressure – consumers are growing more experimental and analytical, weighing price and product benefits over habit or familiarity. The default of sticking with a known brand is giving way to a more deliberate search for the best value.

BEAUTY

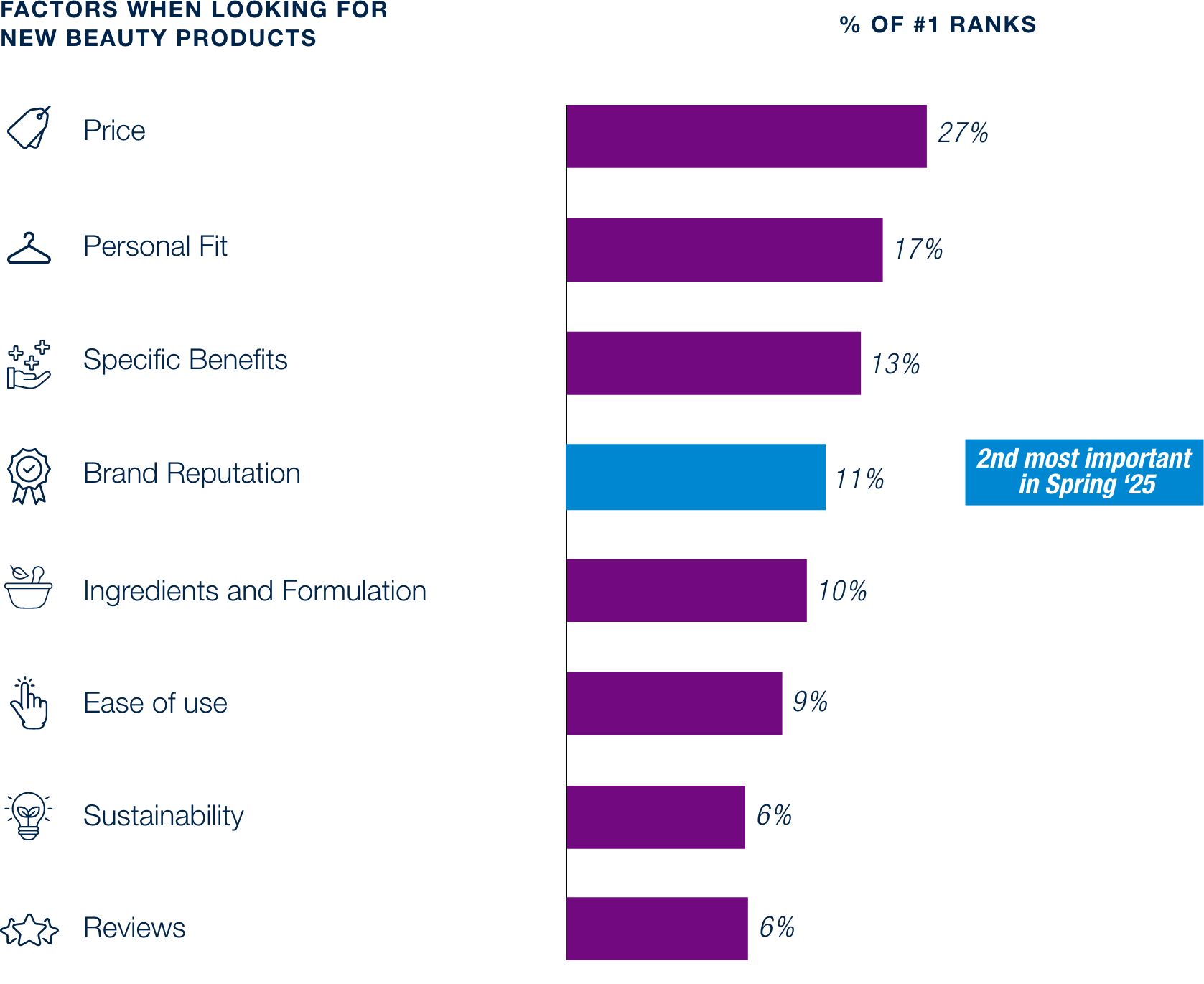

Brand loyalty in beauty is weakening. While brand reputation and trust ranked second among purchase drivers in Spring ’25, it has since dropped to fourth place – behind price, personal fit, and specific product benefits (e.g., anti-aging, hydration). Consumers are increasingly prioritizing what a product does and what it costs instead of the name behind it.

of consumers rank price value & affordability as the most important factor when shopping for new beauty products

Consumers’ Most Important Factor

in Beauty Product Discovery

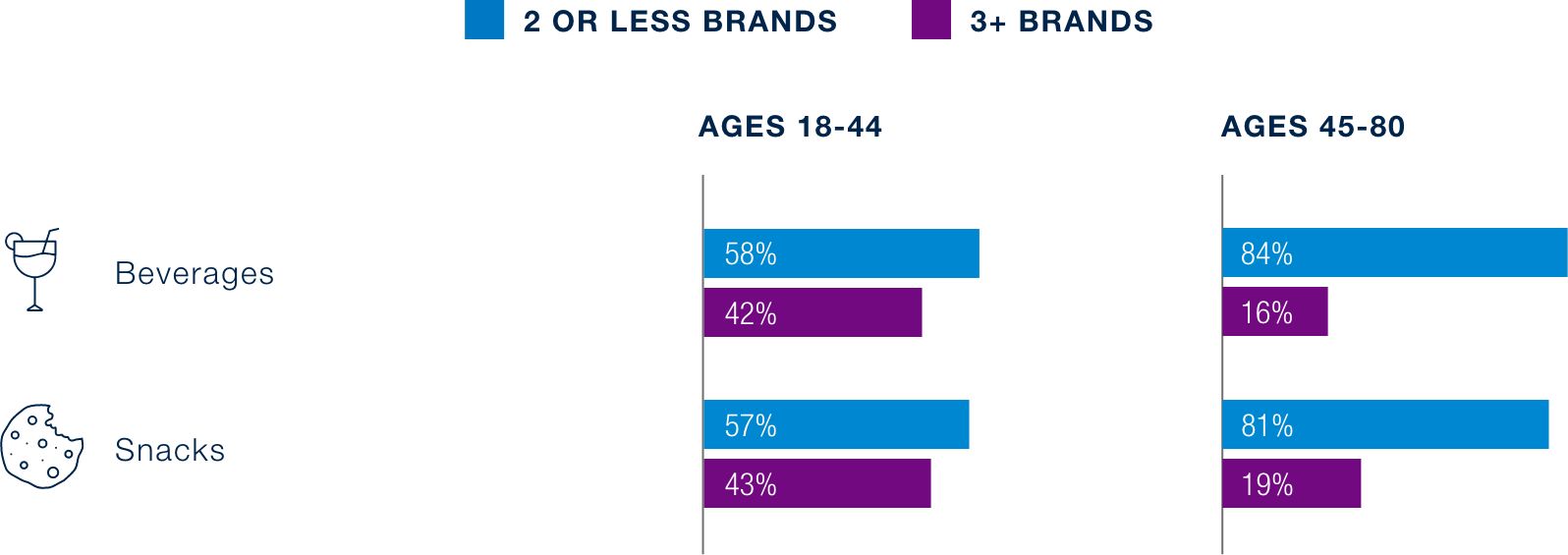

GROCERY (SNACKS + BEVERAGE)

Experimentation is on the rise in snacking. 43% of younger consumers (aged 18–44) purchased three or more brands in the past six months alone – a stark contrast to older cohorts, where 81% purchased no more than two brands in the same period.

GLP-1 users further amplify this trend, showing an 18-percentage point increase in brand trial across age groups, driven by a preference for cleaner ingredients and higher protein options. Together, these dynamics point to a broader shift: consumers actively shopping around to find products that best suit their evolving needs rather than defaulting to familiar brands.

Consumer Experimentation with

Brands in Beverages and Snacks

Number of snack brands tried over the past six months

18% of respondents reported taking a GLP-1

22% of respondents are considering taking a GLP-1

GLP-1 users are less anchored to familiar brands and more driven by nutritional fit, making them highly willing to switch in search of the right product

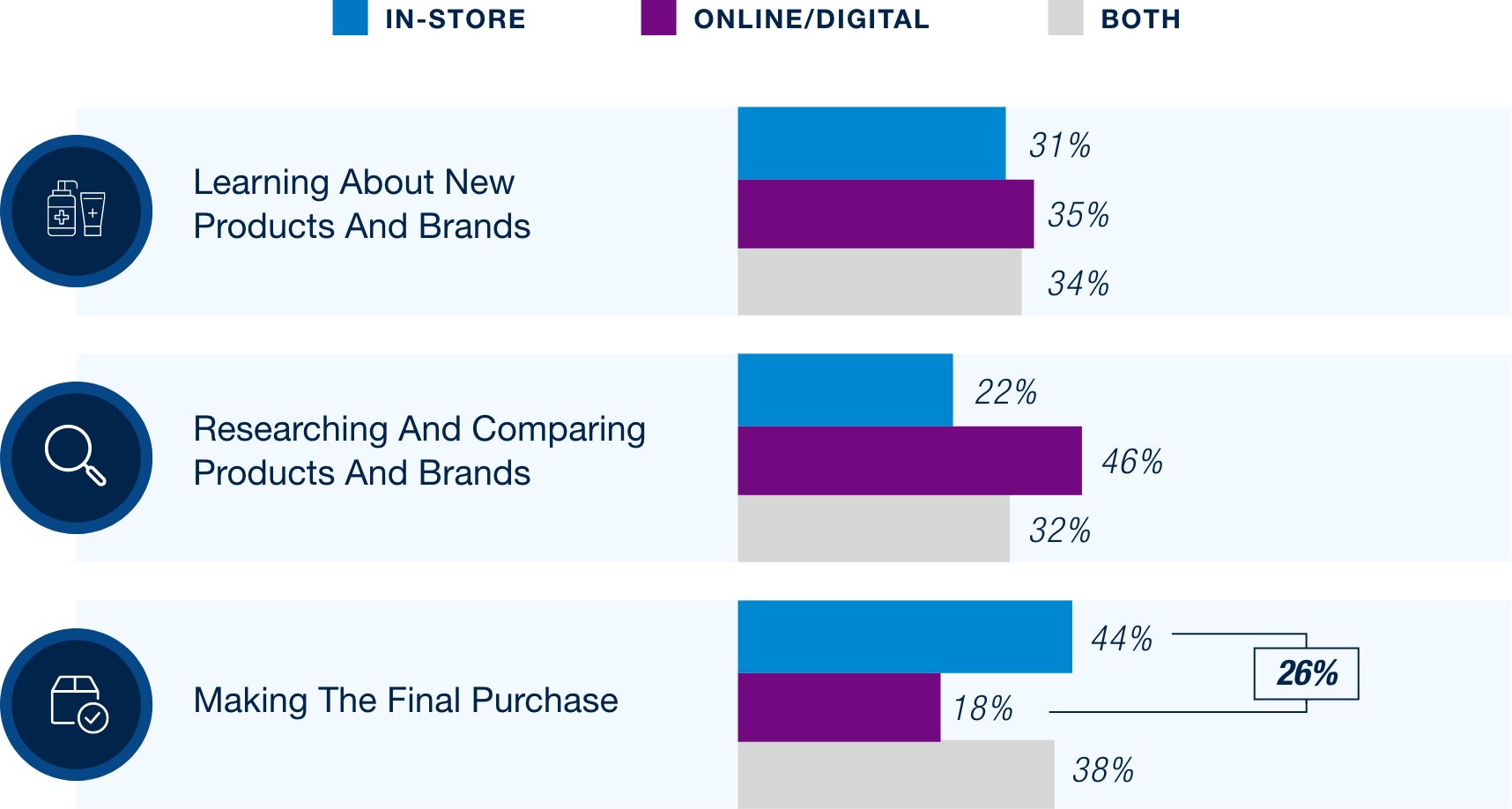

The Evolving Role of Technology in Consumer Decisions

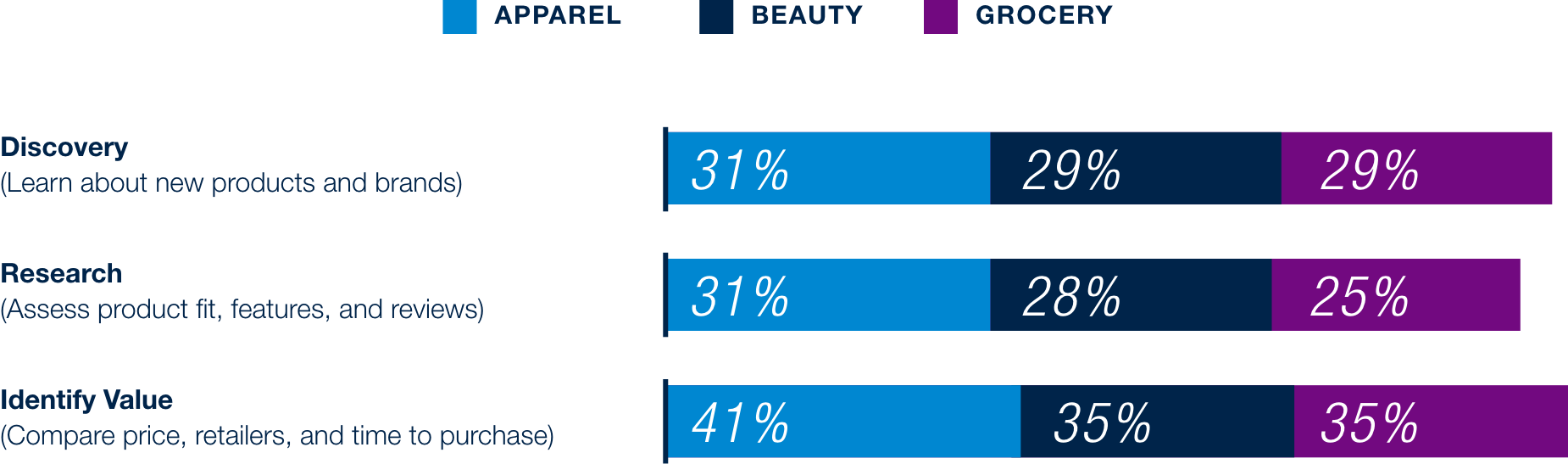

Technology continues to reshape how consumers shop, with online channels taking hold at the top of the funnel – product research and discovery are increasingly happening digitally. That said, the in-store experience still plays a critical role, serving as a final gut check before consumers commit to a purchase.

How Consumers Use AI When Shopping

At which point in the shopping journey is ai leveraged

AI is becoming a fixture across the shopping journey – from product discovery and research to finding the best value. Adoption is consistent across apparel, beauty, and grocery with 25–41% leveraging AI at each stage. Value identification is the most common use case, with shoppers turning to AI to find the best prices and places to buy. This shift is also putting pressure on brand loyalty, as a more analytical approach to shopping makes it easier than ever to comparison shop.

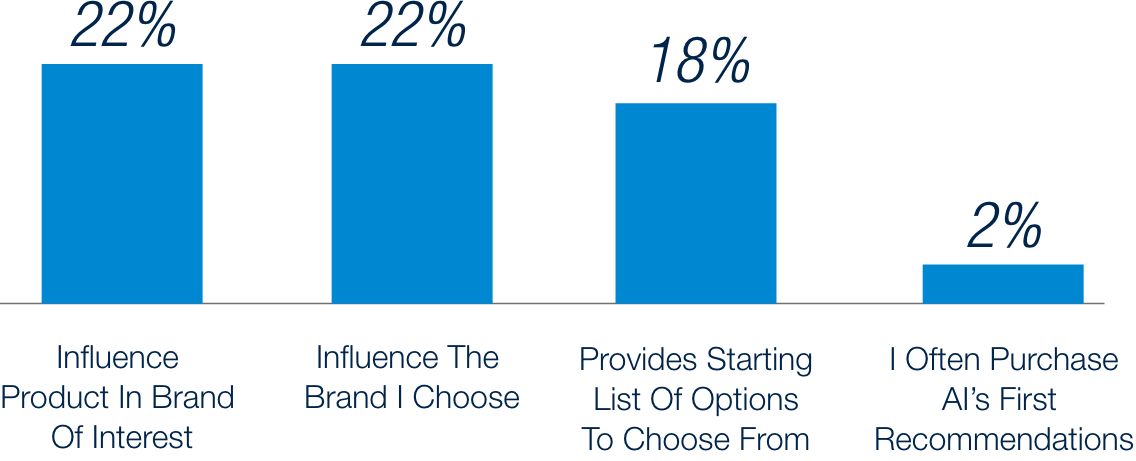

Younger consumers are going further than just using AI as a sounding board when researching a potential purchase. 64% of consumers aged 18-44 ask AI for recommendations and 66% of that group act on them. That level of influence is significant – reshaping the awareness-to-conversion funnel and redefining how consumers find and define value.

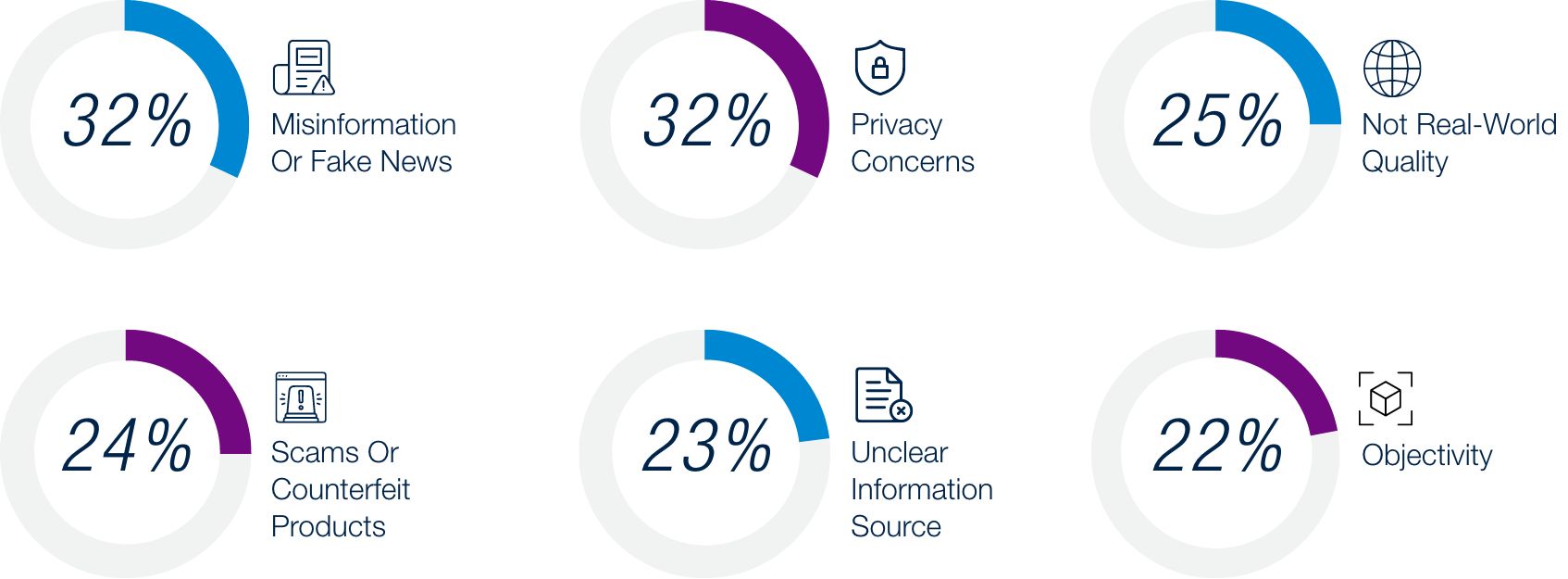

Even with increased AI usage, consumers still have their reservations – particularly around misinformation, privacy concerns, scams, and objectivity of recommendations.

Consumer Concerns around AI

(For <45 year old consumers)

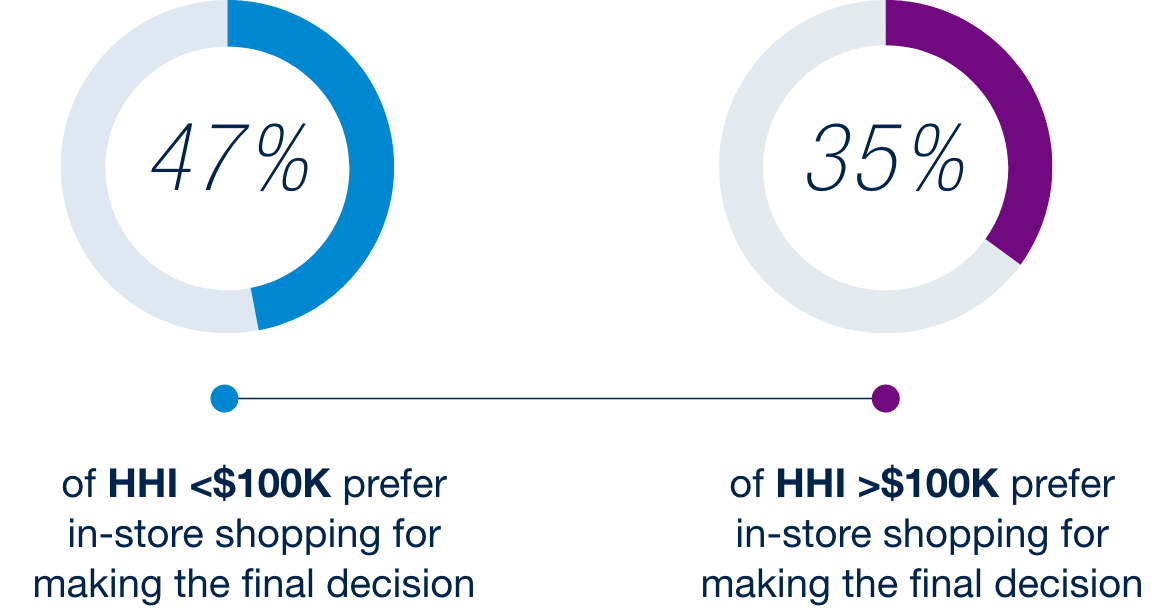

Despite technology’s growing influence in product discovery and research, the store is still the preferred place to buy. 44% of consumers prefer to make final purchases in-store, compared to just 18% who prefer purchasing online. The preference for in-store shopping spans all ages, too. 38% of consumers less than 45-years-old prefer in-store for final purchases, rising to 50% for consumers greater than 45-years-old. Stores remain relevant across all age groups.

Consumer Preferences When

Shopping for New Products

Spotlight on household income for

making the final purchase

Consumers are shifting toward intentional behavior—buying less overall while seeking greater value, quality, and flexibility in how they shop. At the same time, declining brand loyalty and the growing influence of AI and omnichannel journeys are reshaping how purchase decisions are made across categories.

Methodology

Respondents matching U.S. adult population according to gender, age, ethnicity, region & income